A company’s CEO is typically hired based upon a perceived combination of stellar experience and skills. Unfortunately, even some of the best hires make governing their efforts to serve stakeholders difficult by failing to follow best practices in reporting to a board of directors—which call for a detailed written report to be submitted prior to every board meeting.

Simply put, weak CEO reporting creates opaqueness, which can lead boards to make adverse inferences and poor decisions. It can also enable CEOs to mask underperformance or even manipulate information. Proper written reporting, on the other hand, ensures information flow, which is vital for a board to effectively conduct its oversight function.

With clear and robust reporting, misinformation and bias are minimized, and evidence-based decision-making by boards is enhanced. And yet, too many CEOs avoid preparing written reports by instead using emails, oral discussions, or PowerPoint presentations that can obscure clarity. As a result, directors frequently express concerns about the quality, quantity, format, timeliness, and relevance of the information and reporting they receive from the CEO and other management team members.

The good news is that CEOs are accountable to their boards, so reporting shortcomings can be addressed by setting expectations for the CEO, which will cascade to other senior management.

As a governance expert and company advisor, I was recently asked by four boards to draft guidance for what an effective CEO report to a board of directors should contain. This article summarizes these learnings and offers stylistic and content recommendations for a CEO’s report to a board of directors.

Report Purpose, Introduction, Style, and Format

A CEO’s written report is meant to provide relevant, fact-based information, in a full, true, and plain manner, about the performance of the CEO and the organization, while setting out for directors any changes that have occurred since the last board meeting along with variances from financial, strategic, risk, and CEO goals and objectives that have been board-approved.

To assist directors in focusing their reading, an introduction or executive summary should emphasize five or six key points that the CEO wants to convey. This introductory narrative should be short (one page maximum), plain, fact-based, candid, and inviting. If advocacy is occurring, include counterpoints and provide a look-back to help orient board members. Hyperlinks can be used to point directors to key sections of the report relevant to the executive summary.

The report’s style and format should align with the board’s oversight function by supporting transparency, accountability, reading efficiency, and board effectiveness. The CEO should:

- Distribute report to directors at least five working days before the board meeting

- Write in long form, e.g., complete, short sentences, or, if using PowerPoint, ensure that an accompanying oral narrative is not required

- Whenever possible, use headings, colour, directional change arrows, numbers for points being made, and charts and graphs

- Include a table of contents, executive summary, and glossary for company or industry terms and acronyms

- Write in 12 (or more) point, sans-serif, left-justified font

- Avoid long textual passages

- Keep the report factual and evidence-based

- Confer with directors on preferred format and content of the report

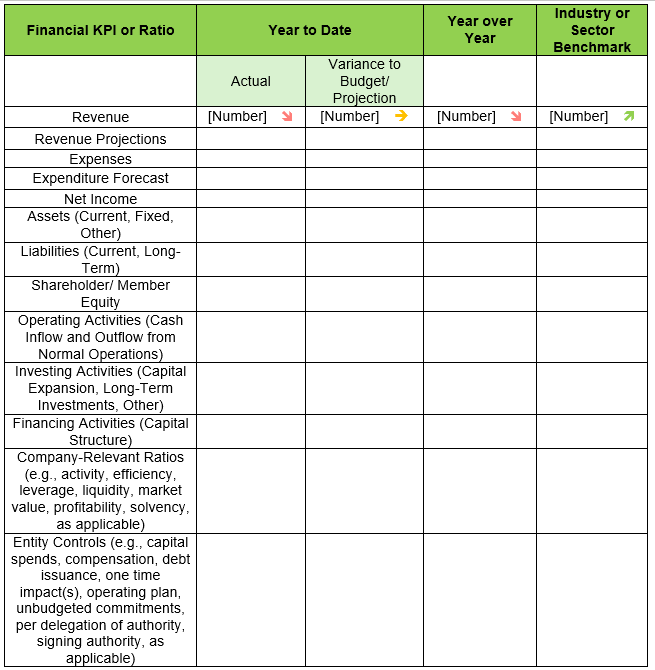

When submitting a written report to a board, CEOs should include best-class dashboards (digital and just-in-time) that cover the following four key areas: financial, strategic, risk, and CEO performance.

Each dashboard should contain user-friendly charts and graphs containing trends. This upfront reporting will enhance and focus discussions during the board meeting. When reviewing these dashboards, directors should not be left to guess why a variance from a board-approved target occurred, so CEOs need to clearly account for any variance being reported. The CEO must own all areas in the report dashboards, even if direct reports will later provide greater detail within the upcoming board meeting.

Financial Dashboard

The arrows and sample key performance indicators (KPIs) in the first column and first row of Table 1 are examples of items and trend analysis that directors should see in a financial dashboard, customized to the organization and approved by the board.

Table 1: Financial Performance Dashboard

As noted above, variances from budget or projection should be explicit and highlighted in the financial performance dashboard. When addressing them in the report, the CEO should take ownership while providing a sense of urgency and outlining steps and a timeline to cure any material or downward trending financial variance.

Strategic Dashboard

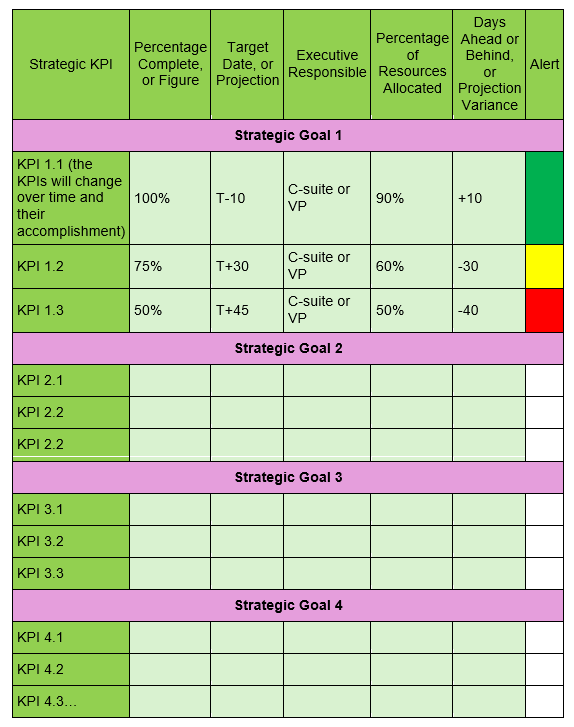

A CEO report should highlight four to seven strategic goals. Examples of strategic goals for a financial institution assisted by the author include: (i) Digital; (ii) Data; (iii) End-User Experience; (iv) Community Impact; (v) Market Share; (vi) Financial; and (vii) Risk.

The sample Strategic Performance Dashboard shown in Table 2 includes four strategic goals and sample cells for the first goal based on percentage complete (rather than a figure), for illustrative purposes. KPIs are specific, time-based end-target measurements, either quantitative or qualitative, or both, that are approved by the board, and that are used to monitor the steady achievement of each strategic goal.

Table 2: Strategic Performance Dashboard

The CEO report should provide context for KPI successes and misses listed in the above dashboard. A plan and timeline narrative for addressing any KPI variance from target should also be provided. In the unlikely scenario that an exogenous unplanned event occurred (e.g., a pandemic, tariffs, other) and prevented or delayed the achievement of one or more KPIs, directors may approve adjusting one or more KPI targets. A board will see the need presumably with the CEO’s early-warning dashboard.

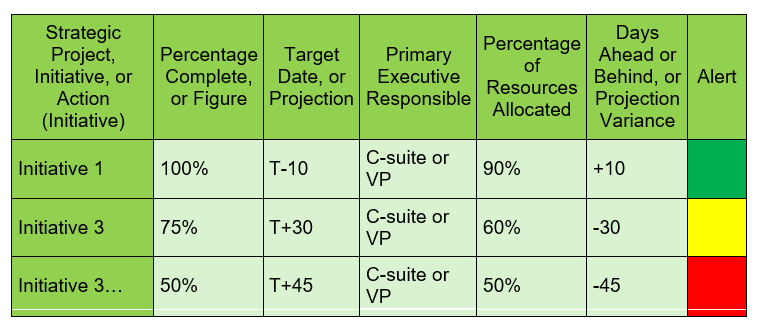

Projects, initiatives, and actions that are necessary to drive the KPIs or are so important that they may become qualitative KPIs in themselves should be listed in a separate chart (see Table 3).

Table 3: Strategic Projects, Initiatives, and Action Completion Plans

Initiatives could span more than one KPI, hence the separate dashboard (Table 3). It is important to add “Primary Executive Responsible” (fourth column in Table 3) for individual accountability and a line of sight by the board.

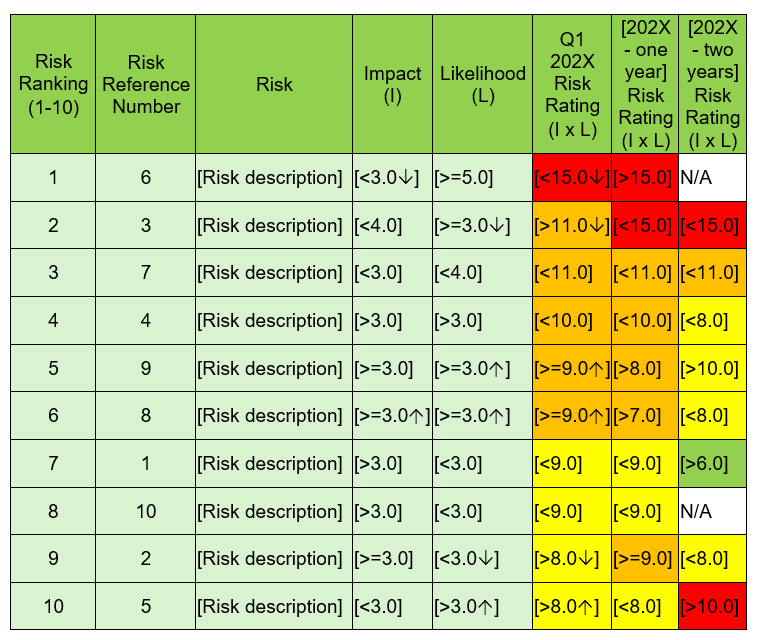

Risk Dashboard

A corporate board should annually approve a risk appetite framework (or the equivalent), including significant financial and non-financial risks, internal controls to mitigate such risks, and assurance that internal controls are effective.

Risks change, emerge, and are dynamic. Internal controls, which mitigate risks, may be unequal in their design and implementation. As a result, it is important for directors to be able to see when changing risks become—or could become—too great. In no particular order, this may suggest a lack of attention by management, or a control weakness, or an exogenous cause.

In Table 4 below, the three columns on the far right provide time context trends.

Table 4: Risk Mitigation Dashboard

A CEO reporting the hypothetical numbers above would address the first five or so highest-ranked risks and set out actions being taken to mitigate them. The CEO might also note learnings from mitigating the tenth-ranked risk (see tenth row in Table 4), given the good work addressing this risk over the last few years. However, because of the use of arrows, directors can see that this tenth-ranked risk is increasing (see sixth column cell with an upper arrow to the right of the “8”), so the CEO should also speak to this, highlighting further action that may be taken.

Furthermore, the CEO may wish to address the seventh-ranked risk with the increases over the last few years (see the decline from green to yellow at the right side of the seventh row), as something to watch, while noting further mitigating actions to be taken.

The risk function may assist in this dashboard and narrative for the CEO.

CEO Goals and Objectives Dashboard

At the beginning of any performance period, a corporate board should establish goals and objectives for the CEO. These may include items such as (i) achieving one or more key strategic goals; (ii) technology implementation; (iii) developing or maintaining important stakeholder relationships; (iv) executive leadership development; (v) board relations; and (vi) personal goals for the CEO, or the equivalents.

The CEO Goals and Objectives Dashboard (see Table 5) forces a CEO to be continuously performance-reflective in writing while serving as an early-warning system for directors. By providing a line of sight that allows boards to access progress without having to wait for the end of a review period, it empowers directors to forestall underperformance concerns and prevent issues from festering. And at the end of the performance period, this dashboard makes it easier for a board to link performance to incentive pay because performance has been tracked. The need to rely on external pay benchmarks is also reduced.

Table 5: CEO Goals and Objectives Dashboard

Top of Mind CEO Issues and Priorities

The financial, strategic, risk, and CEO performance dashboards outlined above provide boards with an important, broad coverage of information necessary to perform their oversight function. But they do not necessarily communicate what a CEO is most focused upon, or believes is most critical, at a reporting point in time. A “Top of Mind CEO Issues and Priorities” section, therefore, is required to focus directors on where they can be of most assistance to the CEO. This is the proverbial “what is keeping the CEO up at night” section of the report. In it, a CEO opens their vest, candidly letting board members know what issues, matters, and priorities are seen as most important by management.

Context for Meeting Agenda Items

The broader board packet may not always provide directors with context surrounding some important meeting agenda items. This section offers procedural fairness to a CEO by providing an opportunity to shape discussions by presenting management’s perspective in advance. This facilitates an on-point constructive and transparent deliberation in the CEO-only session of the board meeting.

Talent Management

This section of the report provides the board with talent- and human resource-related updates. It should include information on any planned or proposed changes to management, key positions, and leadership development, along with information on emergency and permanent talent planning gaps, culture surveys, and labour relations, as applicable.

Organization and Industry Updates

This section is reserved for important organization and industry updates, including the following, in no particular order:

- Noteworthy core activity and organization event updates

- New or emerging regulations and impact summaries

- Technology, digitization, and data integrity updates

- Senior executive updates

- Industry and sector developments

Stakeholder Relations Updates

The fiduciary duty of company directors in Canada extends to consideration of stakeholders, as appropriate, so the CEO’s written report to the board should include a stakeholder section that features the following, in no particular order:

- Community engagement and impact updates

- Creditor updates (including entity-level controls of the organization)

- Customer and supplier developments (including diversification and resiliency)

- Employee, retiree, or pensioner (as the case may be) updates

- Health, safety, and environmental responsibility and enforcement activities

- Investor (or member in the not-for-profit context) engagement and activity updates

Brand, Reputation, and Media Relations

A disciplined approach to intelligence gathering undertaken by management with collective board oversight serves strategic and reputational purposes and can forestall directors from being surprised or misled by something they might read or see in the news. When submitting a report to the board, therefore, the CEO should include a section that highlights any favourable or unfavourable media coverage (including social media) related to the company; its industry; management; and all elements of the organization’s strategic plan, risks, reputation, and brand. This should include article summaries and hyperlinks.

Long-Term CEO Outlook

This section enables the CEO and directors to proceed collectively, while thinking about today, tomorrow, and the future. In it, the CEO should reflect on the shared consensus for the longer term and align management’s current actions with the multi-year strategic plan approved by the board.

Report Conclusion, CEO’s Attestation, Signature, and Date

The conclusion of the CEO’s report should briefly underscore the top five or six key takeaways that management wants directors to receive. In addition to highlighting successes, learnings, and opportunities, it should address performance shortcomings by highlighting cures for any reported variances.

The following CEO attestation should be included, to underscore accountability, reliability, and accuracy, from the CEO to the board:

“This Report is submitted for the Board’s consideration, to the best of my knowledge, information, and belief.”

The CEO should then sign and date the report:

__________________________________________________

[Signature]

President and CEO

__________________________________________________

[Date]

An efficient corporate director may read sections and areas of the CEO report in this sequence: (i) the introduction; (ii) the conclusion; (iii) sections of interest or relevance to the board member’s role; (iv) charts and graphs; and (v) the full body of the report. But regardless of how it is read, a properly written CEO report will:

- Provide enough clarity and facts to support evidence-based decisions being made amid rapid change

- Increase the efficiency of board meetings along with the quality of dialogue with management by enabling directors to arrive at board meetings fully warmed up

- Serve as an early-warning system for underperformance

- Compel management to be disciplined and rigorous in thinking, assumptions, and communications

And if a board determines it is not getting the information it needs to fulfill its oversight role, it really only has itself to blame.

References

Association of Certified Fraud Examiners, Occupational Fraud 2024: A Report to the Nations®, 2024.

Patrice Gelinas, “Questions Boards Should Discuss Before Adding or Modifying ESG Goals in Executive Incentives,” in The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition, ed. Richard Leblanc (Wiley, 2024).

“Key Performance Indicators Infographic,” The KPI Institute, April 9, 2014, https://news.kpiinstitute.org/key-performance-indicators-infographic/.

David F. Larker and Brian Tayan, “CEO Succession Planning,” in The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition, ed. Richard Leblanc (Wiley, 2024).

Richard Leblanc, ed., The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition (Wiley, 2024).

Richard Leblanc, “Model President and CEO Position Description,” in The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition, ed. Richard Leblanc (Wiley, 2024).

Richard Leblanc, “Board Oversight of Possible CEO Misconduct,” in The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition, ed. Richard Leblanc (Wiley, 2024).

Jason Masters, “Financial Literacy and Audit Committees: A Primer for Directors and Audit Committee Members,” in The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition, ed. Richard Leblanc (Wiley, 2024).

Stephen Mallory, “Risk Oversight for Directors: A Practical Guide,” in The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition, ed. Richard Leblanc (Wiley, 2024).

James E. Nevels, “Shareholders, Stakeholder, and Tangible and Intangible Capitals,” in The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition, ed. Richard Leblanc (Wiley, 2024).

Office of Superintendent of Financial Institutions Canada, “Corporate Governance – Guideline (2018),” September 30, 2018, https://www.osfi-bsif.gc.ca/en/print/pdf/node/592.

Michael Useem, “Mission-Critical Checklists for Directors,” in The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Members, 3rd Edition, ed. Richard Leblanc (Wiley, 2024).

About Author

Richard Leblanc is Professor of Governance, Law, and Ethics at York University, editor of The Handbook of Board Governance (Wiley, 2024), and independent advisor to boards of directors.