All businesses have one asset in common—their customer base. Unfortunately, this asset is commonly underutilized because traditional customer segmentation models have a rather limited ability when it comes to unlocking hidden value. Instead of seizing opportunities to extract additional value from their existing customers, too many companies prioritize boosting acquisitions and end up spending far more on targeting new customers than on marketing to the ones they already have.

According to our experience as consultants with Kearney’s Proposition and Customer Experience Labs, companies frequently fall prey to a costly fallacy—the notion of an “average” customer. When segmenting its existing customer base, for example, a financial institution will often employ customer value metrics like monthly revenue per account or average credit card spend per cardholder. But parsing in this manner ignores the Pareto principle, or the 80/20 rule. In this case, the reality is that some 20 per cent of the financial institution’s customers typically contribute around 80 per cent of total value. And by looking at the “average” customer, the business undervalues the most lucrative fifth of the client portfolio while overestimating the growth potential of its remaining customer base.

In addition to looking at the wrong customers, companies often employ stagnant segmentation approaches. Speaking again from our experience in the banking industry, we see many instances in which wealth-based customer segmentation is implemented. At first blush, this can seem like a sound approach, but it fails to incorporate the individual histories of customer–business interactions. It also does not consider the likely future increases in wealth status.

To get the most out of existing customer pools, companies should step back and consider adopting a value-based customer segmentation approach, which provides a quick yet robust method to identify future customer value while enabling companies to develop better growth, retention, and customer maintenance initiatives.

The Mechanics of Value-Based Segmentation

Simply put, value-based segmentation captures the potential revenue-generating characteristics of a customer, using highly relevant attributes. It is also easy to implement, requiring low upfront investment and effort. In working on a customer segmentation effort with an Eastern European bank (for more about this project, see the sidebar “Taking an Avant-Garde Approach to Increasing a Bank’s Revenues” at the end of this article), we identified the following three dimensions that create customer value characteristics:

- Client demographics and financial status

- Product usage, measured in both diversity and depth (e.g., how many products, how much usage)

- Future potential, or expected changes in future net worth and/or usage

Factoring in additional customer attributes, such as psychographic characteristics (e.g., interests, activities, opinions, values) and behavioural attributes (e.g., engagement levels, social media activity), may adjust where an individual customer should be placed along these three dimensions. In sectors where detailed customer demographics and financial information might not be available, attributes like these can help develop a better understanding of clients.

Investing in customer relationships helps to grow the business organically. Consider the example of a recent college graduate who has just opened a basic account at a bank. Such an individual at the beginning of their career typically has little wealth, but is highly likely to build wealth over time. As time passes and they advance in their career, they will look to use other banking products such as a car loan, various forms of insurance, brokerage accounts, and even a mortgage. As long as they are satisfied with their bank, many customers will choose to keep the majority of their business with that institution for the sake of convenience. Therefore, it is important to recognize that a customer with low revenue in the present may offer significant revenue growth potential in the near future. Over time, it is important to build a loyal base of such customers.

Value-based segmentation can serve as a roadmap to help move customers who are part of the 80 per cent that bring in only 20 per cent or so of a company’s business into the smaller grouping that provides significant value. Again, let’s look at an example of how we would implement this method for a bank.

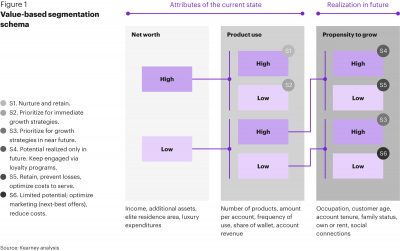

We start by looking at the attributes that describe a client’s current financial status—the net worth dimension. The main aim will be to categorize clients into different net worth clusters. This net worth may include primary or secondary income as well as the value of their liquid assets. In cases where customer income data is missing, net worth can be approximated from information like extreme purchase amounts or other data points (e.g., linked accounts to customers with a known net worth status or having a residence in a high-priced neighbourhood). The net worth dimension is very effective at identifying high-value clients, who typically make up 5 to 20 per cent of a bank’s total client base.

Next, we will look at the product use dimension, which centres on a customer’s activity and level of involvement. The most common attributes here include the number of banking products used by a customer, usage levels per product, frequency of use, account revenues in the past and, where competitor data is available, share of wallet.

To complete the analysis, we will look at the propensity-to-grow dimension, which reflects expectations around how a customer’s value will change over time, either because of the customer’s own income growth or through the depth of engagement they have with a company’s products and services. Figure 1 depicts this particular value-based segmentation process.

Our analysis yields six customer value segments across the value distribution curve.

Highly wealthy and highly engaged customers, the group designated as S1, make up the pool of “ideal customers.” This group will generate a sizeable part of total revenues, but is typically just a fraction of the existing customer base. Customers in this group are already near or at full value with little potential to grow, and thus the focus for this segment should be on retention efforts. Push offers need to be kept to a minimum and they must be personalized. Losing even a single customer in this group will impact the top line.

The second group, S2 (high net worth and low product use), is comprised of customers with the highest growth potential and should be the strategic target for top-line growth. The low amount of activity in this group suggests that these customers use more products and services from a competitor. Each one of these customers that can be poached from the competition increases the size of the highly profitable S1 segment.

The low-net-worth, high-product-use group is fairly sizeable and includes some potential high-value customers. A certain portion of this group, S4, will move to the affluent segment over time. It is important not to lose any of these customers to competitors, so loyalty-related programs would be suitable for this segment. While the rest of this group, S5, will likely remain at their current wealth status, it is key to retain them due to their high level of engagement. Rather than targeting them with sales and marketing activities, efforts should be made to retain them and optimize the cost to serve them, as these customers are already generating as much revenue as can reasonably be expected.

The largest portion of customers is concentrated in the remaining two segments. Segment 3 contains customers who are less wealthy and less engaged today, but who have the potential to be more valuable if they can become more active and engaged users of a company’s products and services. Given these customers’ potential value, investments in developing tailored value propositions are justified for this group. Those in the S6 grouping, on the other hand, will likely stay at the same level of business because they lack the resources to increase their product use. Providing services to these customers through the lowest-cost channels can bring down the cost to serve them while allowing them to reach their fullest revenue-generation potential. Figure 2 provides a visual representation of the value opportunity for each of these segments.

Using Customer Attribute Tracking and Customization for Sustained Segment Value Growth

Our value-based segmentation approach helps to identify segment activation strategies based on current data, which reflects past and present-day customer activity. However, to consistently increase customer value we need to track changing customer attributes over time and update offers to them accordingly. Most companies tend to identify their customer segments and put forth fixed offers, failing to update and personalize their strategies based on changing customer attributes.

There is a strong need to implement a mechanism for customer attribute tracking to update the offers being made to each segment. Continuing our example about a recent college graduate with little present-day wealth but significant future earnings potential, Figure 3 shows how our value segmentation approach allows a bank to track the changing life stages of this customer. The bank can adopt the relevant activation mechanism to move the customer from the “low value” segment to the “ideal customer” status, which offers the highest value.

While our approach can identify what mechanism is required to maximize the value of each segment, segmentation does not provide information on detailed customer behaviour, preferences, and needs. In-depth customer insights from ethnographic studies, social listening, and existing market intelligence data can be combined with the value-based segmentation process to develop tailored propositions and drive consumers toward higher profitability.

When the future value potential of an existing pool of customers is uncovered using value-based segmentation, businesses can make major strides toward providing truly differentiated offerings to this key asset. Properly leveraging the new insights obtained through such an effort can help to develop emotional connections via targeted marketing efforts that increase customer loyalty and boost their value to the business over time. It all starts by identifying which customer segments to invest the most in and channeling resources in an optimal way.

TO RECEIVE IBJ CONTENT ALERTS, SUBSCRIBE ON OUR HOMEPAGE.

SIDEBAR: An Avant-Garde Approach to Increasing a Bank’s Revenues

At the end of 2019, a market-leading retail bank in Eastern Europe embarked upon a journey to become more customer-centric. At the time, the bank counted more than 50 per cent of its country’s population among its customers, but it was losing customer value to new banks. In order to grow, the business needed to retain and protect its customer base, boost its client portfolio value by addressing single-product clients, and switch from a transactional to a long-term, relational client approach. Doing so would require it to identify the high-potential customers in its existing base and then tailor its strategies to activate them.

Unsurprising in light of the 80/20 rule, 87 per cent of the bank’s revenues were being generated by a mere 20 per cent of its retail clients. Nearly half of the client base had not been included in previous segmentation efforts, and almost 30 per cent of the bank’s revenue came from these customers. In addition, the bank’s previous segmentation work was not value-driven and did not capture the growth potential of different segments.

Our approach focused on identifying growth opportunities. Customer wealth, product penetration and usage, and age became the three building blocks to determine which segments were most worth investing in. We ultimately identified five segments by value potential:

- Superstars: High affluence and/or abnormally high usage

- Avant-Garde: Affluent with limited product usage

- Basic: Mass with transactional behaviour

- Sunset: Older customers from mass wealth segments with specific product categories

- Risk and Uncertainty: Customers with delinquencies and unpredictable behaviour

The “avant-garde” segment, which represented around 20 per cent of the bank’s customer base, was found to have the most potential, as it consisted of wealthy and mass affluent individuals with low product usage. We saw an opportunity to triple revenues from each customer in this segment.

Following focused customer research, we designed and tested a number of propositions, including tailored product bundles, personalized campaigns, and loyalty incentives. Market testing of the new propositions allowed us to forecast an increase in incremental net revenue of approximately 15 per cent per year from these high-potential customers.

About Author

Tatiana Goncharova is a Kearney consultant affiliated with the firm’s Proposition and Customer Experience Labs, which brings big customer ideas to life to deliver rapid and sustainable growth for clients. Contact: Tatiana.Goncharova@kearney.com.

Tushar Sharma is a Kearney consultant affiliated with the firm’s Proposition and Customer Experience Labs, which brings big customer ideas to life to deliver rapid and sustainable growth for clients. Contact: Tushar.Sharma@kearney.com.

Vladimir Lukin is a Kearney consultant affiliated with the firm’s Proposition and Customer Experience Labs, which brings big customer ideas to life to deliver rapid and sustainable growth for clients. Contact: Vladimir.Lukin@kearney.com.