A recent study of 275 professional portfolio managers reported that the ability to execute strategy was more important than the quality of the strategy itself (“Measures That Matter,” Ernst & Young, Boston, 1998). Strategy implementation was the most important factor shaping these portfolio managers’ assessment of management and corporate valuations. This finding seems surprising, since for the last two decades, management theorists, consultants and the business media have focused on how to devise strategies to generate superior performance. Apparently, strategy formulation has never been more important.

Yet, other observers concur with the portfolio managers’ opinion that the ability to execute strategy can be more important than the strategy itself. In the early 1980s, a survey of management consultants reported that less than 10 percent of effectively formulated strategies were implemented successfully (Walter Kiechel, “Corporate Strategists Under Fire,” Fortune, Dec. 27, 1982). A 1999 Fortune article, in a cover story of prominent CEO failures, concluded that the emphasis placed on strategy and vision created a mistaken belief that the right strategy was all that was needed to succeed. The authors concluded that “…in the majority of cases—we estimate 70 percent—the real problem isn’t [bad strategy]…it’s bad execution.” (R. Charan and G. Colvin, “Why CEOs Fail,” Fortune, June 21, 1999). Thus, with reported failure rates in the 70- to 90-percent range, we can appreciate why sophisticated investors have concluded that execution is more i m p o rtant than good vision.

WHY ORGANIZATIONS HAVE DIFFICULTY IMPLEMENTING STRATEGY

Strategy expert Michael Porter describes the foundation of strategy as the “activities” in which an organization elects to excel. If the foundation of strategy is, as Porter maintains, the “selection and execution of hundreds of activities,” then strategy cannot be limited to a few people at the top of an organization (Michael Porter, “What Is Strategy,” Harvard Business Review, November/December 1996).

Strategy must be understood and executed by everyone. The organization must be aligned around its strategy, and performance management systems help create that alignment. Herein lies one of the major causes of poor strategic management. Most performance management systems are designed around the annual budget and operating plan. They promote short-term, incremental, tactical behaviour. While this is a necessary part of management, it is not enough. You cannot manage strategy with a system designed for tactics. It is our belief that it is this need—the need for strategic enterprise management—that has been driving the widespread adoption of the Balanced Scorecard.

THE BALANCED SCORECARD: A NEW APPROACH TO IMPLEMENTING STRATEGY

The simple idea behind the Balanced Score c a rd Concept (BSC), which we first introduced in a 1992 Harvard Business Review article, is that an organization’s strategy must be translated into terms that can be understood and acted upon (R. Kaplan and D. Norton, “The Balanced Scorecard: Measures That Drive Performance,” Harvard Business Review, January/February 1992). A BSC uses the language of measurement to more clearly define the meaning of strategic concepts like quality, customer satisfaction and growth. A scorecard that accurately describes the strategy can serve as the organizing framework for the management system.

Organizations that were early adopters of the Balanced Scorecard have shown impressive results to date. Consider the following case studies:

Mobil Oil (U.S. Marketing & Refining Group). The BSC was introduced in 1993 to help manage Mobil’s transformation from a highly centralized, production-driven oil company to a decentralized, customer-driven retail organization. The results were rapid and dramatic. By 1995, Mobil had moved from last place to first in industry profitability. It maintained this No. 1 position for five consecutive years, through its merger with Exxon in October 1999. From a negative cash flow of $500 million (all currency in U.S. dollars) in 1992, Mobil USM&R recorded a positive cash flow of $900 million in 1998.

Cigna Insurance (Property & Casualty Group). The BSC was introduced in 1993, one year after Cigna P&C had been the most unprofitable company in its industry segment. Its new CEO used the BSC to help manage Cigna’s transformation from a money-losing generalist to a “top-quartile specialist,” focusing on niches where it had a comparative advantage. Again, the results were rapid and dramatic. Within two years, Cigna had returned to profitability. This performance was sustained for four consecutive years; in 1998, Cigna P&C’s profitability placed the company in the top quartile of its industry. The division, nearly bankrupt five years earlier, was sold to an international insurance firm in December 1998 for more than $3 billion.

Brown & Root Energy Services (Rockwater Division). The division president introduced the Balanced Scorecard to the management team in 1993 to help clarify and gain consensus on the strategy for two newly merged engineering companies. The new strategy transformed the division from one competing solely on price, selling engineering hours on cons t ruction projects, into one that could formulate price based on the value it contributed to its targeted customers. The scorecard-design process built the new management team, identified attractive new customer segments, new views of the customer value proposition, and gained consensus on the new approach for moving forward. By 1996, Rockwater was first in its niche in both growth and profitability.

Chemical Retail Bank (now Chase Bank). The BSC was introduced in 1993 to help the bank assimilate an acquisition, to introduce more integrated financial services, and to accelerate the use of electronic banking. The BSC clearly defined the strategic priorities and provided a structure to link strategy and budgeting. In the space of three years, profitability increased by a factor of 20.

These four examples illustrate the power of the BSC approach. These executive teams successfully executed their strategies when the majority of their colleagues could not. But the speed with which the results were achieved spotlights the potential that exists for every organization. The capabilities for success were already present in these organizations, which had achieved their breakthrough results with the same people, the same facilities, and mostly the same products and services. People already had the skills and knowledge needed to execute the strategies. But they lacked focus, alignment and an understanding of where the organization was trying to go. The BSC eliminated these barriers and provided the focus that unlocked the strategic skills and knowledge of the organization.

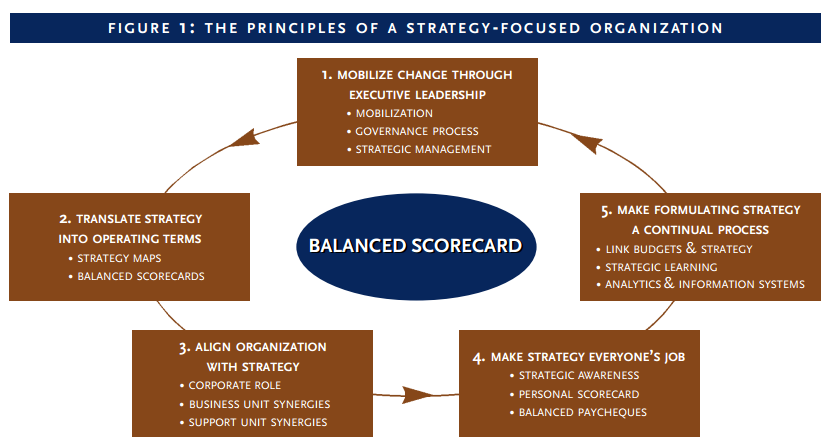

Companies that successfully implement scorecards reinvent every part of their management system to focus on strategy. This is a significant departure from traditional management programs that link performance to financial frameworks—budgets or even newer shareholder value approaches (or non-financial frameworks like Total Quality). The successful organizations created a performance-management program that put strategy at the centre of its management processes. Our continuing research has revealed a set of five principles (see Figure 1) that permit organizations to become strategy-focused, enabling them to execute their strategies rapidly and effectively.

1. MOBILIZE CHANGE THROUGH EXECUTIVE LEADERSHIP

A successful BSC program starts with the recognition that it’s not a “metrics” project, but a “change” project. The single, most important condition for success is the ownership and active involvement of the executive team. Strategy re q u i res change from every part of the organization. If those at the top are not energetic leaders of the process, change will not take place and the opportunity will be missed.

John Kotter describes how transformational change must begin at the top, with three discrete actions by leaders. The leaders of successful BSC programs clearly followed this model (John Kotter, Leading Change, Harvard Business School Press, 1996).

Establish a sense of urgency. Before change can occur, the organization must be “unfrozen” to understand why dramatic change is needed. In the case studies presented above, the companies were experiencing difficult and challenging times. The need for change, apparent to executives at the top, was not always apparent to the rest of the organization. People were comfortable with the status quo. They needed to accept that change was necessary and inevitable if they were going to be able to generate the benefits of a new strategy. The first step in the change process for each of these organizations was making the need obvious to all.

Create the leadership team. The dynamics of the executive leadership team usually determine whether the BSC succeeds. The leaders of successful BSC adopters recognized that their current collection of functional specialists had to be transformed into a strategically focused, cross-functional, integrated team. Members of executive teams tend to view management issues from their individual, functional perspectives. These executives often have surprisingly little awareness of how other functions work.

Each of the early adopters supplemented their traditional executive team with managers who were experts on the strategic issues. The new strategies at Mobil and Chemical Bank were based on customer segmentation. Both companies added a marketing executive to an executive leadership team that had previously consisted of functional and business unit heads. The addition of new perspectives was critical in breaking down the traditional barriers to teamwork that had existed at the top.

Develop the Vision and Strategy. The creation of a shared vision and strategy was an effective way to build an executive leadership team (in contrast to a collection of individual business unit heads who met periodically to discuss business issues). The framework of the BSC guided the team in its development of a new vision and strategy. A tremendous amount of cross-fertilization took place as each element of the strategy was adapted to the score card format. At Mobil, the strategic issues surrounding customer segments (marketing), yield optimization (manufacturing), cost of capital (finance), and supply-chain management (transportation, pipeline) became the shared issues of the executive team. Historically, each of these issues was considered the domain of a single functional executive.

2. TRANSLATE STRATEGY INTO OPERATING TERMS

Putting strategy at the centre of the management system implies that strategy can be described so that it can be understood and acted upon. Unfortunately, there are no standards for strategy. If we are going to build management systems around strategies, we need a discipline for describing strategy that is both reliable and consistent.

The Balanced Scorecard provided that discipline for the successful organizations. In addition to building scorecards, the process helped executive teams to better understand and articulate their strategies. The foundation of the design is a Strategy Map, shown in Figure 2, which defines the “architecture” of the strategy. The description begins with the financial perspective of the shareholder (or appropriate key constituent in non-profits). It defines the relevant long-term indicators of success (e.g., ROI, shareholder value) and divides it into a long-term (growth) and a short-term (productivity) component.

The revenue-growth strategy requires a specific value proposition, in the customer perspective, that describes how the organization will create differentiated, sustain-able value for targeted segments. Different value propositions and different target customers result from different strategies. In general, we find three types of value propositions in practice: price, relationship and innovation. (Michael Treacy and Fred Wiersma, The Discipline of Market Leaders, Addison-Wesley, 1995). The design of the internal perspective links internal business processes to the customer value proposition. The value chain of the organization can be divided into three or four generic processes: innovation, customer management, operations/logistics and regulatory/society. Finally, the learning and growth perspective defines the competencies, technologies and climate required to support the unique demands of the customer value proposition and the internal processes.

Once the Strategy Map has been defined and agreed on by the executive team, designing a scorecard that measures and targets is a straightforward process. The Strategy Map approach highlights the fact that Balanced Scorecards should not just be collections of financial and non-financial measures, organized into four perspectives. In fact, Balanced Scorecards should reflect the strategy of the organization. A good test is whether you can understand the strategy by looking only at the scorecard and its Strategy Map. Strategy scorecards, along with their graphical representations on strategy maps, provide a logical and comprehensive tool to describe strategy. It communicates clearly the organization’s desired outcomes and its hypotheses about how these outcomes can be achieved.

3. ALIGN THE ORGANIZATION WITH THE STRATEGY

The BSC is a powerful tool to describe a business unit’s strategy. But organizations consist of numerous sectors, business units and specialized departments, each with its own operations and often its own strategy. If synergy is to occur, the strategies across these units should be coordinated. The BSC can and should be used to define the strategic linkages that integrate the performance of multiple organizations. This is not an easy task. Functional departments, such as finance, manufacturing, marketing, sales, engineering and purchasing, have their own bodies of knowledge, language and culture. Functional silos arise and become a major barrier to strategy implementation, since most organizations have great difficulty communicating and coordinating across these functions. For organizational performance to be more than the sum of its parts, individual strategies must be linked and integrated. The corporate role defines the linkages expected to create synergy and ensures that the linkages actually occur.

Figure 3 shows the linkages at the Mobil North American Marketing and Refining division. The high-level strategic themes (in No.1) guide the development of the Balanced Scorecards in the business units (in No.2) that are either geographic regions or product lines, such as lubricants. Each unit formulates a strategy appropriate for its target market in light of the specific circumstances it faces (competitors, market opportunities and critical processes) but that is consistent with the themes and priorities of NAM&R. Without corporate prompting, these joint activities typically don’t take place. The Corporate Scorecard provides the communication and coordination mechanism across business unit scorecards. The measures at the individual business unit levels do not have to add to a corporate or divisional measure, unlike financial measures that aggregate easily from subunits to departments to higher organizational levels. The business unit managers choose local measures that influence, but are not necessarily identical to, the corporate scorecard measures.

Beyond aligning the business units, strategy-focused organizations must also align their staff functions and shared service units, such as human resources, information technology, purchasing, environmental and finance (No.3 of Figure 3). Often, this alignment is accomplished with a service agreement between each functional department and the business units. The service agreement defines the menu of services to be provided, including their functionality, quality level and cost. The service agreement becomes the basis of the Balanced Scorecard constructed by the functional department. The department’s customers are the internal business units, the value proposition is defined by the negotiated service agreement, and the financial objectives are derived from the negotiated budget for the department. Next, the department identifies the internal process, and learning and growth objectives that drive its customer and financial objectives.

When this process is complete, all the organizational units—line business units and staff functions—have well-defined strategies that are articulated and measured by Balanced Scorecards and strategy maps. Because the local strategies are integrated, they reinforce each other. This alignment allows synergies to occur so that the whole exceeds the sum of the parts. Linkages can also be established across corporate boundaries (as in No.4 of Figure 3). Several companies constructed Balanced Scorecards to define their relationships with key suppliers, customers, outsourcing vendors and joint ventures. Companies use such scorecards with external parties to be explicit about (1) the objectives of the relationship, and (2) how to measure the contribution and performance of each party in the relationship by factors other than price or cost.

4. MAKE STRATEGY EVERYONE’S JOB

Sources have estimated that approximately 50 percent of all work performed in industrialized countries today is knowledge work. Workforce knowledge re p resents an asset that we are just beginning to use effectively. In this structure, strategic information and decision-making can no longer be limited to executives and senior managers. Knowledge workers make strategic choices every day. Successful BSC users took steps to ensure that everyone in the organization understood the strategy, was aligned with it, and capable of executing it. Traditional human resource systems and processes played an essential role in enabling this transition.

Communication and education to create awareness: A prerequisite for implementing strategy is that all employees understand the strategy. A consistent and continuing communication program is the foundation for organizational alignment. No single medium is sufficient to transform everyone’s understanding of the strategy. It must be conveyed in all communication media and vehicles and reinforced by the personal behaviour of executives.

Personal alignment: All of the successful BSC users aligned individuals with the strategy through personal goal-setting processes; some have even created personal scorecards. Setting objectives for individuals, of course, is not new. Management-by-Objectives (MBO) has been around for decades. But MBO is distinctly different from the kind of alignment achieved with the BSC. The objectives in an MBO system are established within the structure of the individual’s organizational unit, reinforcing narrow, functional thinking. The individual objectives established within the framework of the BSC are cross-functional, longer-term and strategic.

Incentive compensation: Those who implemented the BSC successfully moved quickly to link incentive compensation to targeted scorecard measures. This linkage unleashed powerful forces. Most successful BSC users ultimately conclude that, to modify behaviour as required by the strategy and as defined in the scorecard, change must be reinforced through incentive compensation. When the BSC is linked to the incentive compensation program, there is a visible increase in the level of interest in the details of the strategy.

5. MAKE FORMULATING STRATEGY A CONTINUAL PROCESS

Most organizations build their management processes around the budget and operating plan. The monthly management meeting reviews performance versus plan, discusses variances from past performance, and requests action plans for dealing with short-term variances. Such tactical management is necessary, but in most organizations that is the only thing management does. Besides the annual strategic planning meeting, no meeting occurs where managers discuss strategy. We surveyed participants at conferences and learned that 85 percent of their management teams spend less than one hour a month discussing strategy. Companies with the BSC adopt a new “double-loop process” to manage strategy. The process integrates the management of tactics with the management of strategy, using three important processes, as depicted in Figure 4.

First, organizations link strategy to the budgeting process. They use the Balanced Scorecard as a screen for evaluating potential investments and initiatives. Companies usually have an operating budget that authorizes spending for producing and delivering existing products and services, and marketing and selling them to existing customers. These organizations now introduce a strategy budget to fund initiatives that will develop entirely new capabilities, reach new customers and markets, and make radical improvements in existing processes and capabilities. This distinction is essential. Just as the Balanced Scorecard attempts to protect long-term objectives from short-term sub-optimization, the budgeting process must protect the long-term initiatives from the pressures to deliver short-term financial performance.

The second step in making strategy formulation continual is to introduce a management meeting to review strategy. As obvious as this step sounds, such meetings didn’t exist in the past. Now, management meetings are scheduled on a monthly or quarterly basis to discuss the Balanced Scorecard, so that a broad spectrum of managers come together to monitor organizational performance against the short-term targets for the scorecard’s financial and non-financial measures. The managers check whether strategic initiatives are being implemented as planned. On the surface, the process is similar to the typical monthly operating reviews. However, instead of reviewing only financial performance, managers now review the performance of, and take corrective actions for, all the measures on the Balanced Scorecard. The process creates a focus on strategy that did not exist before.

Information feedback systems change to support the new management meetings. Many organizations create an open reporting environment in which performance results are made available to everyone in the organization. Building upon the principle that “strategy is everyone’s job,” they empower “everyone” by giving them the knowledge needed to do their jobs. At Cigna Property & Casualty, a first-line underwriter saw performance reports before a direct-line executive if she happened to be monitoring the feedback system. Such open sharing of strategic information creates a set of cultural issues that revolutionize traditional, hierarchical approaches to information and power.

The third and final step for making strategy development continual sees a process evolve for learning and adapting the strategy. The initial Balanced Scorecard represents hypotheses about the strategy; at the time of formulation, it is the best estimate of the actions expected to create long-term financial success. The scorecard-design process makes the cause-and-effect linkages in the strategic hypotheses explicit. As the scorecard is put into action and feedback systems begin their reporting on actual results, an organization can test the hypotheses of its strategy to see whether its strategy is working. Some, like Brown & Root and Sears, did the testing formally, using statistical correlations between measures on the scorecard to determine whether, for example, employee empowerment programs were increasing customer satisfaction and improving various processes. Others, like Chemical Bank, tested the hypotheses more qualitatively at meetings, where managers validated and refined the programs being used to drive service quality and customer retention. Mobil’s EVP Bob McCool commented on the difference:

“In the past, we were a bunch of controllers sitting around talking about variances. Now we discuss what’s gone right, what’s gone wrong. What should we keep doing, what should we stop doing? What resources do we need to get back on track?”

A new kind of energy is created. People use terms like “fun” and “exciting” to describe the meetings. One senior executive reported that the meetings became so popular that “there was standing room only and he could have sold tickets to them.”

Companies also use the meetings to search for new strategic opportunities that aren’t currently on their scorecard (see Henry Mintzberg, “Crafting Strategy,” Harvard Business Review, July/August 1987, and Gary Hamel, Leading the Revolution, Harvard Business School Press, 2000, for discussions of emergent strategy). Events can occur that were not anticipated at the time the strategy and scorecard were conceived. Ideas and learning emerge continually from within the organization. Rather than waiting for next year’s budget cycle, the priorities and the scorecards are updated immediately. Much like a navigator guiding a vessel on a long-term journey, constantly sensing the shifting winds and currents and constantly adapting the course, the executives of successful companies use the ideas and learning generated by their organization to fine-tune their strategies. Instead of being an annual event, strategy formulation, testing and revision become a continual process.

BEING STRATEGY-FOCUSED

The Balanced Scorecard has enabled organizations to introduce a new governance and review process, one focused on strategy, not tactics. The new governance process emphasizes learning, team problem-solving and coaching. Review meetings now look into the future, exploring how to implement strategy more effectively, and identifying the changes that need to be made in the strategy—based on what has been learned from the past.

This is a management process attuned to the needs of contemporary businesses. The essential ingredient is a simple framework and tool that allows strategy to be articulated clearly. Without such a strategic framework, there can be no strategic management system. The Balanced Scorecard is the heart of the management system that strategy-focused organizations will use to build their future.

This article is adapted from an article originally published in the Balanced Scorecard Report, a newsletter published jointly by the Balanced Scorecard Collaborative and Harvard Business School Publishing. It summarizes material contained in the authors’ book, The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment, Harvard Business School Press, 2001.